Intro

Key Stats

The business

Bull Case

Bear Case

Business metric highlights

Finances

Conclusion

1. Intro

Covid has impacted many different industries and businesses in many different ways. Underlying consumer behaviour has changed at a pace almost never seen before, with a much greater focus on ‘at home’ products/services. This has forced some industries to pivot and re-think their long-term direction. For others it has presented an opportunity to accelerate their growth trajectory.

“An exercise bike with an iPad” isn’t an uncommon response whenever I search the company on twitter. For a long while, this was my overarching opinion – a company/brand solely based around an exercise bike (old technology) combined with a touch-screen interface. What I didn’t fully understand was the cultural significance of the brand, the problem the product solved, the stickiness of the ecosystem and the powerful ‘community’ pull that live sessions have.

Peloton might currently be viewed as just a hardware company, however the software and creation of ecosystems to accompany the hardware is where the future lies.

I love this quote from an article on Peloton “Though we are isolated in our homes, we are bound together through a shared tactile experience with the product: thousands of legs twirling at the same pace, thousands of fingers twirling the knob just so. Part of the hypnotic appeal of the Peloton instructor monologue is how seamlessly the commentary slips into jargon about cadence and resistance. Through their physical prowess, the instructors lay claim to a broader social and even moral authority, and their classes suggest that the act of using the Peloton itself releases positive energy into the world.”

2. Key Stats

Market Cap: $32B

1.67M Subscribers (+134% y/y)

TTM Revenue: $2.95B up 140% y/y

Total platform workouts: 113M from 26M y/y

21 avg monthly hours per user (+67%)

CAC at $505 down from $1,150 in 2018

92% retention rate

3. The business

The idea

The idea is simple. What if you can access a live workout from the comfort of your own home, without going through the process of booking days in advance and being restrained by the limitations of the physical infrastructure? This is where Peloton comes in.

The company’s mission is to, “use technology and design to connect the world through fitness, empowering people to be the best version of themselves anywhere, anytime.” They use their interactive software platform to offer a connected/immersive fitness experience.

The products

Peloton bike & bike+: These two options start £1,750 and offer a high-quality bike with a built-in adjustable screen (allowing for floor exercises).

Tread: The Peloton tread starts at £2,295 and is a well-built treadmill with a shock absorber rubber belt, touchscreen, and sound system. The screen also rotates to allow floor-based exercises.

Accessories + Apparel: Accessories include bike clips, weights, waterbottles, headphones and much more. Whilst Apparel includes branded peloton workout gear.

Software ecosystem: Each of the machines comes with the Peloton software eco-system built in. This provides all of the data on your performance, allows you to interact with the community, and includes all of the live and on-demand workouts.

A sub-sector of this software is the Peloton digital subscription which doesn’t require the user to own a physical piece of peloton equipment. The platform offers a variety of workouts, yoga, meditation, running and much more.

4. Bull Case

The Brand

The Peloton brand is undeniably strong. Like Apple or Nike, people want to be associated with the company in one way or another. You could even argue the company are somewhat of a cultural phenomenon – celebrities are clamoring to get an endorsement from Peloton.

This ‘cult-like’ aura adds to the appearance of exclusivity which, in turn, adds to the potential pricing power. The product is a status symbol, and with status symbols, you can typically end up charging whatever the hell you like.

Stickiness

The Peloton Connected Fitness Subscription, which makes up the majority of revenues, has an astounding 92% retention rate (similar to that of Netflix). Put simply, if you take 100 Peloton subscribers and return to them 12 months later, 92 of those customers will still be active on the Peloton service. This indicates a low churn and therefore a ‘sticky’ product that people come back to again and again.

In addition to this, Peloton products represent a high initial ‘sunk-cost’ ranging from about $1.9k up to $4.3k. This high sunk-cost raises the mental barrier for switching products.

Q2 Average Net Monthly Connected Fitness Churn was 0.76%;

Q2 12-month retention rate was 92%.

Both these numbers are incredibly strong and indicate a product that people love to use. Compare this to the ~50% retention figure for traditional gyms and you can see a clear driver for long-term profitability stemming from recurring revenues.

Network effects

The product sells itself. Peloton is more than a bike - it's a service & an experience. You are being trained by a world class instructor and competing against friends in the comfort of your home. There is a large amount of on-demand and live content available which members can completely digitally immerse themselves in.

All of this creates a scenario where you get the feeling of being in a genuine group workout.

The more participants involved, the greater the competition, motivation, and sense of community. The opportunity cost of members leaving becomes high.

Leadership

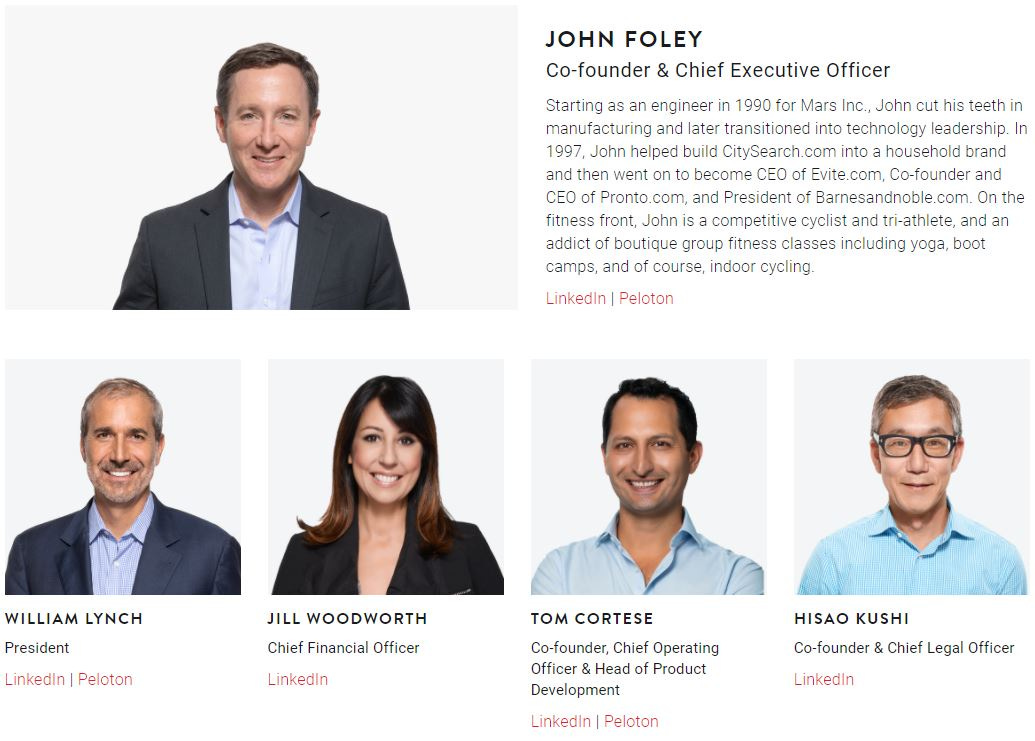

John Foley, along with three co-founders (Tom Cortese, Hisao Kushi & Yony Feng) had the goal to create an immersive indoor cycling experience. As of today, the company also features 33 international experts who are influencers, experts, brand ambassadors, and member advocates.

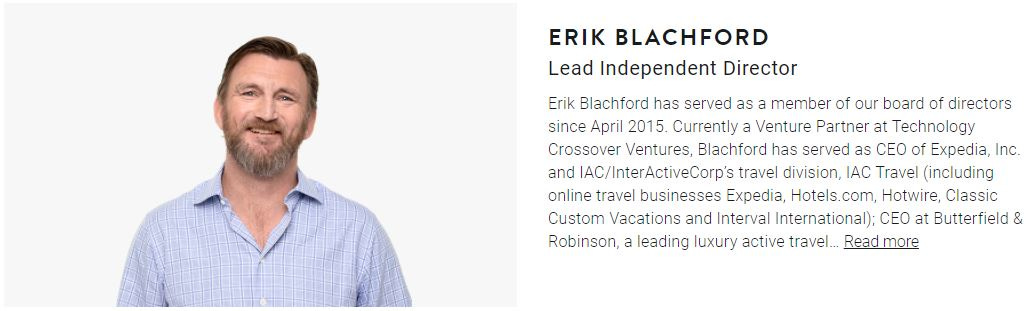

The team offers valuable experience for the customers and strategically for the business - for example, Erik Blachford (Lead Independent Director) has important connections to the travel and leisure industry, which is an area I can see Peloton targeting in the near future.

Market Size

The global fitness industry is a notoriously tricky industry to get involved with. Recent stats show that only 20% or people go to a gym, and included in this 20%, 50% quit each year. This leaves 80% of people who don’t go to a gym.

John Foley, co-founder and CEO of Peloton Interactive Inc, says the total addressable market is close to 200 million gym goers worldwide, and the company’s growth rate can go up to 100 times before it may slow down.

Global health and fitness industry expected to grow due to increased awareness of health and rising costs of healthcare.

Based on the research that Peloton has conducted, the market for Connected Fitness products is massive.

Peloton's TAM is 67M households, of which 45 million are in the United States. Within this, they estimate 52M are interested in learning more about the connected fitness products without seeing the price.

Out of the 67M households that are interested in Peloton's connected fitness products, 14M households (12M in the US and 2M rest of the world) are interested in Peloton's products at its current price points.

On top of a large TAM, Peloton seems to be expanding its market: based on a 2019 Member Survey, 4 out of 5 members were not in the market for home fitness equipment before they purchased a Peloton equipment.

The market for Peloton's Digital subscription is huge if we compare it to a few other large streaming services:

Netflix: 204M subscribers

Spotify: 155M subscribers

Disney+: 100M subscribers

Hulu: 40+M subscribers

Based on the above, Peloton's market for subscription memberships could easily be in the range of 100-200M subscribers. Which is crazy, and leaves a lot of room for growth.

Apparel

The apparel aspect of the business is led by Jill Foley, the wife of Peloton founder and CEO John Foley. The company choose not to break out it’s apparel sales - it’s folded into the company’s connected fitness divitsion.

“It has never been a strong revenue driver, but it’s a way for the company to entice new sign-ups for its app-based membership via referral codes that offer clothing discounts. In the past, Peloton has noted that apparel sales are often offset by those referral discounts and other annual markdowns.”

Peloton is on track for an estimated $60M+ in apparel sales this year, a number that took Lululemon almost a decade to reach.

“By working with partners like Adidas, Peloton stirs up more interest in its brand and gives its subscribers access to exclusive content. Peloton said it will hold a series of on-demand classes beginning Thursday to commemorate the Adidas partnership. The company will also hold a special live class on March 25”

Convenience

The $PTON killer feature is time. People don’t want to commute if they can move from sitting on the couch to working out in less than 10 steps.

Innovation

The company are constantly innovating with new business models, new partnerships, new ways of exercising. A company that is constantly innovating is exactly what I want to see.

Below is just one example of an innovation that focuses on the gamification of workouts. Just watching this got me pumped up.

Partnerships with celebs/companies

Leading on nicely from innovation is the partnership with artists within their workouts.

Peloton are creating a bunch of high-profile artist-themed workouts. Some of these include…

Bad Bunny

Beyonce

Billie Eilish

Burna Boy

Lady Gaga

Dolly Parton

Megan Thee Stallion

This is such an interesting model and concept as the upcoming releases will probably be featured, which will amplify their streaming numbers. In my opinion this is just the beginning for artist relationships with Peloton…

These huge boost in artist numbers after live events can somewhat be compared to the Travis Scott live event in fortnite, where the event boosted streams for his album release “the day that he released new single "The Scotts," with Kid Cudi, at midnight ET, after it premiered during the set -- Scott racked up 24.4 million U.S. on-demand streams of his songs”.

Other artists will be clamoring to get featured on a Peloton workout.

Connected Fitness as a trend

Connected Fitness as an experience is here to stay. I think the majority of people who own a Peloton device will continue to use it once the pandemic is over. Connected fitness is a trend that I feel is here to stay.

Data

I’m not certain on the levels of data currently being collected by the Peloton products, however there is an opportunity here. Connected fitness, along with wearable technology is steadily becoming mainstream. And with this, the more data a company can gather on their users, the more they can utilise the data moving forwards. I believe Peloton could have an incredibly valuable set of data on their hands.

The way in which they choose to monetize this data is something I’m not sure of, but I’m sure we will find out over the coming years.

Acquisitions

Only recently Pelaton announced the acquisition of Precor, a leading global manufacturer of commercial fitness equipment, for $420M.

Precor is one of the world’s largest suppliers of commercial fitness equipment and gives Peloton the opportunity to have its equipment in hotels and standalone commercial gyms.

Precor embodies the Peloton mission of putting Members first. Over the last few months, we've gotten to know the team and saw firsthand how much they care about their products, customers and, last but not least, their employees. By combining our talented and committed R&D and Supply Chain teams with the incredibly capable Precor team and their decades of experience, we believe we will be able to lead the global connected fitness market in both innovation and scale," said Peloton's Lynch.

In addition to this, a flurry of acquisions was only just reported.

“Peloton purchased Aiqudo in February, as well as Atlas Wearables and Otari late last year, according to Bloomberg. The exercise company said the acquisitions were meant to improve both talent and technology.”

“All three deals give Peloton the ability to possibly build new hardware and services that expand on its bikes, treadmills and software services, Bloomberg reported. The deals could also help Peloton debut its own digital voice assistant, with the engineers joining the company focused on AI and computer vision technology.”

5. Bear case

Human nature

For this one, I would say the odds are stacked against any sort of company attempting to get people to exercise on a regular basis.

Exercising somewhat goes against our natural urges/desires, and we can see this in some of the statistics surrounding exercise and gym memberships, e.g. 50% of people cancel after the first 6 months.

Many companies have tried similar solutions to Peloton and many have failed. I would argue, however, that Peloton are coming a at the problem from a different angle – one focusing more on community and togetherness, which is something that other replicas have failed to achieve.

Insiders selling stock

Courtesy of @AndrewRangeley

Argument to be made against this is that, as a $PTON employee who has seen your shares 10X over the past year – why would you not sell? It’s the prudent thing to do.

What really happens post-covid?

There is a huge lingering question-mark over Peloton as a company and as a product. Post-covid, are we still going to be using at-home exercise bikes or will we attempt to go back to physical gyms? At the moment Peloton is focusing on the subscription model, however with the acquisition of Precor we could see the company moving more towards the commercial space and getting their equipment into gyms/hotels etc. This strategic shift could unlock heaps of currently untapped revenue potential.

Too expensive, will never reach mass adoption

It’s a pricey product, for sure. However I don’t think it’s particularly unreasonably priced if you factor in the multiple value aspects e.g. convenience, cost saving from travelling, curated workouts, professional instructors, personal fitness data… the list goes on.

Though, for many, this product will simply be out of reach.

Wait times

Peloton CEO John Foley said the company’s production capacity grew 700% over the past year and that supply of its exercise bikes is close to meeting demand.

Unfortunately for Peloton, there is somewhat of a logistical challenge involved in getting these heavy, fragile items safely out to the buyers in a short period of time. Part of the problem is the level of growth experienced over the past year – the company were simply not prepared.

“Our manufacturing output has significantly increased, and we’ve officially begun ramping up production at our new Shin Ji factory in Taiwan. Unfortunately, well-publicized West Coast port delays and COVID-related factors continue to present challenges to returning our delivery times to pre-pandemic levels. We are making substantial additional investments in the near-term to address our extended delivery times and are hopeful that an acceleration in vaccine distribution and the broader opening of our economy will provide a tailwind to our efforts over the coming months.”

Competition

Peloton are not the only ones in this line of business, believe it or not. Connected fitness is fast becoming a serious industry – with companies like Apple jumping on the bandwagon. Some examples of serious competition within the industry include:

Apple $9.99 p/m for home workouts

ICON Similar product

Nautilus

Zwift

Equinox Owns fitness boutiques, gyms and the SoulCycle brand. Entering ‘at home’ fitness.

Lululemon Acquisition of Mirror – steam live workout classes.

Tonal At home gym fitness equipment.

Adaptiv Trainer-led contend for ‘at-home’

I’m sure there are many more. But these are all companies operating within the same industry. I believe the distinguishing factor between Peloton and these other companies is the strong brand. If Apple fully get into this space then peloton may run into some trouble. Alternatively, it’s not inconceivable someone like Apple simply buy’s out Peloton.

6. Business Metric highlights

Retention Rate

Firstly, let’s look at the retention rate for Peloton. They have an extremely strong retention rate on their connected fitness subscription of 92% as of Q2 2021. In real terms, this means that if 100 customers purchased a ‘connected fitness subscription’ at this time last year, 92 of those would still be using the product today. Compare that figure to gyms and it’s clear to see the stickiness of the product.

Customer acquisition cost

We can define the CAC as Sales & marketing costs divided by the total number of ‘connected fitness subscriptions’ added that year. Just to note here, for 2021 we can only use the numbers for the first two quarters, but that should give us a good idea of how the year is progressing thus far.

2018 = $1,150

2019 = $1,220

2020 = $823

2021(Q2) = $505

In my eyes, these results are seriously strong as it shows the continued strength of the brand over time. In other words, it now takes less than half the advertising spend to convince someone to buy a Peloton bike than it did 4 years ago.

Subscribers

Connected Fitness subscriptions is a subscription service that Peloton members signs up to alongside the purchase of one of the physical products (e.g. either a bike or a treadmill). The connected fitness subscription number has been growing rapidly over the past several years, with the end of Q2 2020 reporting a 134% y/y growth to 1.67 million. Alongside this, the number of digital fitness members grew 472% to 625,000 members. And lastly, the total members currently stand at 4.4Million.

Engagement

These metrics are crucial as they measure the level of engagement with the Peloton product, which is the leading indication of retention.

“Total platform workouts (both Connected Fitness and Digital) grew to over 113 million in the quarter from 26 million in the year-ago quarter. In Q2, we recorded our largest single day of Member workouts (over 1.6 million).”

“In Q2, Average Monthly Workouts per Connected Fitness Subscription was 21.1, representing 67% year-over-year growth. Users with Connected Fitness Subscriptions logged over 98.1 million workouts, up from 24.3 million workouts in the same period last year, representing 303% year-over-year growth.”

7. Finances

Mkt Cap of $32B

TTM Revenue of $2.95B up from $1.23B Y/Y. This includes revenues of $1.06B in just the last quarter, almost beating the entirety of the previous year period.

Q2 Revenue $1.065 billion +128% YoY

Connected Fitness Revenue $870 million +124% YoY

Digital Subscription Revenue $195 million +152% YoY

Connected Fitness Membership base 1.67 million +134% YoY

Net income $63.6m vs net loss of $55.4m YoY

Churn Rate of 8%

Revenue

Peloton operate on a different financial year end date to most companies, so these aren’t technically the FY results, but the Q2 results.

In the most recent quarter, peloton have generated $1064.8 million which represents 128% y/y growth. This number almost reaches the total TTM revenue from 2019 of $1.23 billion, indicating impressive growth.

From 2017 to 2020 the company has grown at a rate of 99%, 110% and 100% respectively – starting at $218.6Million and ending at $1.825Billion. *note this does not include 2021 as we are only half way through this period*.

The revenue is split into two main aspects on the financial statements – connected fitness products, and Subscription. Somewhere included in this is the sale of apparel, but this isn’t explicitly outlined.

Profitability

Interestingly, Peloton have only just started to become profitable as a company, reporting a trailing twelve month net income of $166.40 Million compared to the previous year’s TTM net loss of ($191.2) Million.

It’s common for growth companies such as peloton to be essentially losing money whilst they are in the growth phase of their life-cycle. This is why it’s so encouraging to see Peloton hit profitability at this point. It shows the success of the business model at scale and that the company are here to stay if they can maintain this level of profitability.

Balance Sheet

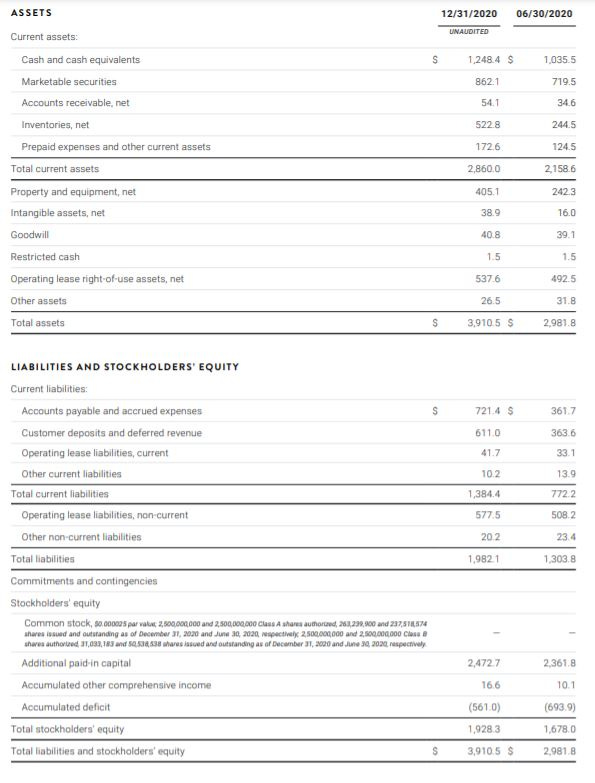

As of the end of 2020, Peloton’s cash position looks healthy. $1.25B in cash and cash equivalents (or $2.86B in total current assets) is sufficient to meet the level of debt on the balance sheet considering the total liabilities is $1.98B.

Valuation

Peloton are flying high at the moment, especially when you zoom out to over several years - pre-pandemic. The company are currently trading at a P/S ratio of 11.91, down from their all-time-high of 20.51 at Christmas time (2020).

Comparing the stock to Nautilus, who's P/S ratio is at 0.99 it’s hard to argue Peloton stock isn’t expensive. Especially since Nautilus stock has seen a rise of 1,219% since this time last year, compared to Peloton’s 380% gain in the same time-frame.

I love the business model and the product, but I have serious reservations about the current price.

8. Conclusion

Peloton is more than a bike - it's a service & an experience. You are being trained by a world class instructor, competing against friends, all within the comfort of your home.

Overall, I’m far more interested in the company after doing my research than I was before I started – this is usually a good sign. An even better sign is that I really want to spend the best part of £2k on an exercise bike with an ipad…

Peloton as a business is an interesting proposition. The bull list is compelling…

Strong brand

Sticky product

Powerful flywheel effect

Excellent leadership

Large TAM

Optionality

Data

Smart acquisition

Low churn

…the list goes on.

All of these points have to be considered within the context of the inherent risks that the Peloton business model has to deal with. There remains some fairly substantial question marks regarding the future feasibility of the connected fitness model, the long-term desire for at-home fitness and the company’s ability to continue to grow outside of a global pandemic.

Even taking into account the fact that Peloton are currently trading at high multiples, I believe the value the company offers over the long-term is worth the risk. Sometimes a strong brand is all you need to succeed. But if you couple a strong brand with smart leadership and a sticky product – the sky is your limit.

Looking towards the future, if Peloton can continue to innovate, expand internationally, devise a more affordable pricing model/product and diversify their content - then I am confident in their continued success story.

Cheers,

Innovestor

P.S. thanks for taking the time to read. If you enjoy these articles and would like to donate, the button below should take you to a buymeacoffee.com donation page. Thanks!

Absolutely meticulously reports. Thanks sir 👍