Thesis

Key Stats

Background

Why Lemonade

Conference Call

Risks

Core financials

Valuation

Conclusion

1. Thesis

Lemonade at their core are a disruptive technology company with 3 main competitive advantages.

The global shift to digital solutions has (and will continue to) accelerate the growth within Lemonade’s line of work, as clients are looking for end-to-end digital experiences. The current insurance market leaders will have trouble pivoting to this model if proved to be successful, as a large proportion of their agents would no longer be needed.

Premium per customer – the future growth prospects of Lemonade somewhat rely on their ability to increase the ‘Premium Per Customer’ (PPC) number. Over time, they will need offer a wider array of options for each customer and focus on higher-ticket items such as homeowner insurance. Some of this will naturally take place as renters move to buy their first home and stick with Lemonade.

Data – the ability to acquire and utilise data in the current business landscape cannot be underestimated. Data is the digital gold. There is immense value in the data Lemonade collects, which will ultimately give them the edge over traditional industry models with regards to underwriting, acquiring and retaining customers.

2. Key Stats

Hit the million customer milestone

Homeowners/pet insurance up to 40% of new business in Q4 2020, up from 33% in Q4 2019

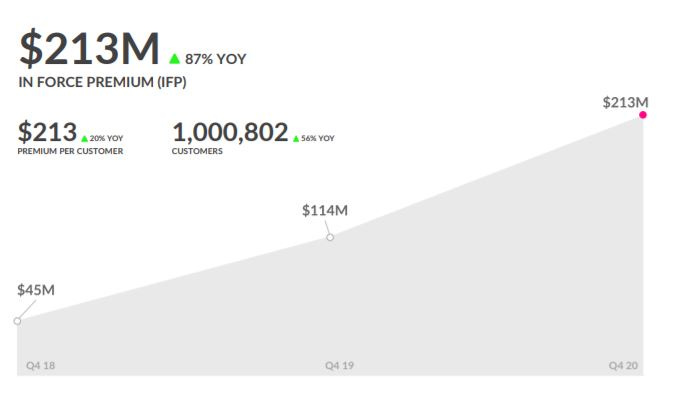

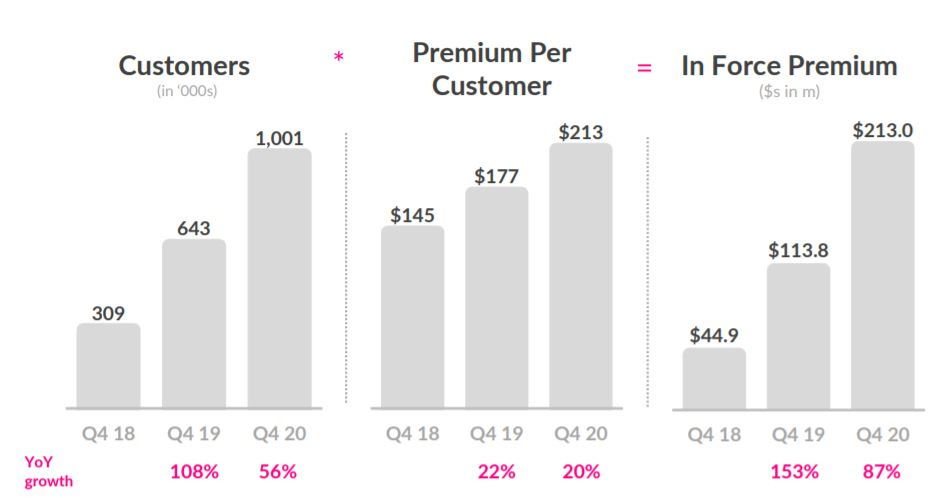

In force premium up 87% to $213M

Premium per customer of $213 (20% increase y/y/) and marks third sequential quarter of accelerating growth.

Each dollar invested represents 88% more IFP growth y/y

3. Background

What they do

Lemonade are aiming to re-imagine the experience of purchasing insurance by leveraging technology, data, AI, design and behavioural economics in order to become the “worlds most loved insurance company”. They are deliberately positioning themselves as an anti-insurer, and are outwardly focused on making insurance fun again.

The company leverage growing technologies such as big data and artificial intelligence in order to allow the company to strip out a large proportion of the overhead costs usually associated with making a quote.

Below is an example of the various tasks throughout the business being completed by code/algorithms/bots.

AI Maya – Onboarding and customer experience bot, uses natural language to guide customers through an easy and fun process of joining Lemonade. Maya handles everything from collecting information and personalizing coverage to creating quotes and facilitating payments securely. By asking customers a limited number of high-impact questions, and adapting based on their responses, AI Maya is able to dramatically reduce onboarding times while still collecting and utilizing the data that is central to our continuous improvement.

AI Jim – AI Jim handles the entire claim through resolution in approximately a third of cases, paying the claimant or declining the claim without human intervention (and with zero claims overhead, known as loss adjustment expense, or LAE). AI Jim assigns claims he is not authorized to settle, or ones where he identifies concerns, to human claims experts, analyzing each expert’s specialty, qualifications, workload, and schedule to determine to whom to assign the claim.

CX.AI – Their customer support bot. It handles a third of customer inquiries.

Forensic graph – Their fraud detection platform.

Blender – An insurance management platform that facilitates collaboration throughout the organization.

Cooper – An automation bot that handles repetitive tasks.

They are a full-stack insurer, meaning they underwrite policies and process claims. Their main value lies in a quick and pain-free buying experience for the user. The company also have a giveback program which donates excess premiums to a charity of the policyholder’s choice.

How they make money

The way Lemonade makes money is relatively simple and doesn’t differ greatly to traditional models. The customer pays a premium to the insurance company under the agreement to pay for claims covered under the customer’s specific policy.

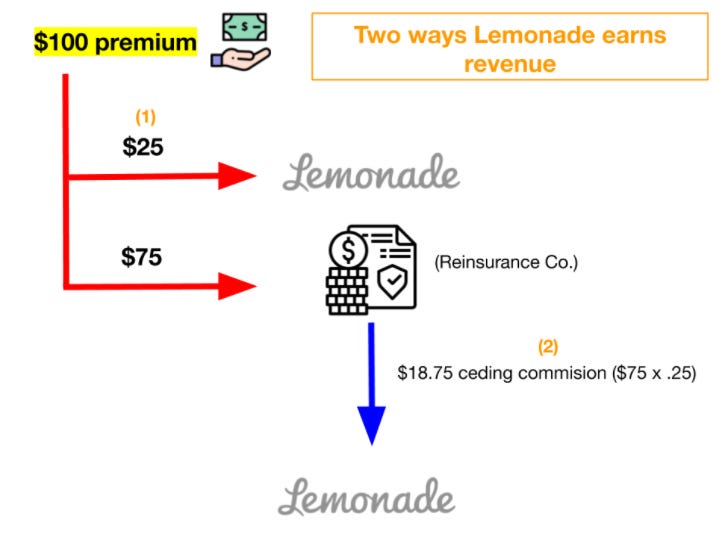

There are 3 main revenue sources:

1. Retain a fixed fee which is usually 25% of premiums. The remaining 75% of the fees goes to the re-insurance company.

E.g. if Lemondate quote you $100 as a premium for your cover, Lemonade will keep $25 (25%) as a fee for finding the business.

2. Earn a ceding commission of 25% for every dollar ceded.

E.g. of the $75 ceded to the re-insurance company, Lemonade will keep $18.75 as a seeding commission.

3. Investment income Net investment income represents interest earned from fixed maturity securities, short term securities and other investments, and the gains or losses from the sale of investments.

Lemonade raised more than $500 million from their 3 million shares issued. Looking to invest in increasing their insurance suite offering by getting into things like life insurance. Expanding growth with some dilution.

4. Why Lemonade?

Data

Data will be one of the most valuable commodities within the next 20 years. If a company can find a way to collect large volumes of high-quality data, they can then utilize it in the future to cut costs and further improve their service. Data is an important aspect for Lemonade, and is one of the factors hoping to give them an edge within underwriting.

Q4 Updates

Lemonade keep delivering on their earnings. In the 4th quarter of 2020 we saw customers grow from 643,000 in 2019 to 1,001,00 in 2020 (+56% growth). Reaching the million customer mark is a huge feat, and something that took other insurers decades to achieve. This, if nothing else, proves there’s something special in this product.

In addition, the strategy of acquiring customers cheaply through the renters insurance business with the intention to retain and increase the LTV (Lifetime Value) via cross sales, upsells, and graduation to homeowner insurance.

Growth

The company continues to grow at an impressive rate – providing 3 consecutive quarters of accelerating growth. This can be shown by the In Force Premium number which is the number of customers multiplied by the premium per customer. This is important as it captures the fact that…

Lemonade are diversifying their product mix across a broader suite of products, and…

The existing customer base is expanding.

Secondly, the company have expanded to reach the entirety of the US. With the aim to look into Europe next. They offer at least one product in all 50 of the US states, up from 27 since IPO.

Customer satisfaction & trust in the brand

This one is crucial and often underestimated with regards to the importance of the continued success of Lemonade’s business model. Part of this retention rate or customer satisfaction rating can be seen by looking the ‘graduation’ numbers. That is, renters becoming homeowners and increasing their premiums. This number grew by about 250% y/y.

Utilising technology (AI)

One of the most innovative aspect of the Lemonade service is the high reliance on the AI bots to do most of the heavy lifting usually carried out by humans. This is a potential game changer in the industry as it lowers the standard overheads usually present in the acquisition of business. This strategy allows Lemonade to effectively compete with other incumbents in the industry.

Interestingly, normal insurers may ask about 20 questions to collect 20 data points. Here though, Maya asks considerably fewer questions but still collects thousands of data points, which is an incredibly important point. And it can readily store all that collected data far more easily and quickly than a human.

5. Conference call

Here I’m just going to draw out a few main points made from the conference call. There’s a lot to unpack, so I’ll keep it as brief as possible.

Our 2020 annual loss ratio was 71% as compared to 79% in the prior year. We've now seen an incredibly healthy loss ratio for the year as well as healthy loss ratios across all four quarters and all four seasons affording confidence that even as we grow fast we are growing profitably.

Cautious underwriting resulted in not feeling the impact of black swan events such as the Texas Freeze. There shouldn’t be too much impact on 2021.

Global expansion

We think of our market as global. We don't expend too much thought about which state or which country our sales occurring. Our machine is trained to invest its incremental dollar in whichever channel offers the highest ROI at any given moment. So it takes into account using machine learning models likely churn, expected claims, projected up sells and it derives from these predictive lifetime value which then compares to the anticipated customer acquisition cost in that channel. This results in optimal and increasingly improving LTV to CAC ratios and it also dictates a ranking of products and campaigns that are being promoted based on the ROI for the incremental dollar spend.

In terms of expanding into new markets like the UK or Asia, I'd say a couple of things. The first is that we have an expansive vision for Lemonade. We think that our cocktail, value proposition of great value strong values and delightful product is a cocktail that enjoys universal appeal and therefore it's a question of when not if with regard those new geographies.

New products

So as with new geographies our ambition for new products is expansive. We want to cater to all our customers’ needs and to become attractive to an ever-growing universal customers and new products are really an essential component in achieving this. In our S1 prospectus for IPO we included an illustration of our prototypical Lemonade customer. We showed a young woman who joins at age 25 and all she has is a bike and some personal belongings and then we showed how we could grow with her as she goes through predictable life cycle events as she collects pets and human dependence and she adds valuables and vehicles and homes and our product roadmap is developing in the service of this strategic vision of ours. And in terms of car insurance in general and the Tesla related question in particular let me say the following. The entire mobility space is going through unparalleled dislocations. Ride sharing is increasingly competing with car ownership while autonomous vehicles promise to transform the nature of how risk is allocated in the car industry. If a Tesla crashes while on autopilot that could arguably be characterized as a faulty product issue rather than a faulty driver issue and they therefore may be better handled under rubric of product warranty than car insurance.

So this is one of the many revolutions and transformations of the digital age and these kinds of transformations put incumbents on their back foot and they create tremendous opportunities for innovation for companies that don't have a legacy business to protect. So we follow these dislocations with keen interests but for now that's all I'm going to say on this topic. Thank you for that question.

Crypto

To-date we haven't seen compelling applications for blockchain or crypto currencies at Lemonade but it's a fast-moving space and we're entirely open and even excited at the prospect of that changing and in terms of our investments our most high conviction investment is in LMND and we plan to deploy as much of our cash into our own business as we can profitably do.

Of course, in the meantime we will invest the cash that we don't need right now but we certainly don't plan to make sizable investments and efforts as volatile as Bitcoin. The opportunities in front of us are massive and we want to keep our powder dry and dependably available.

The Machine

Question

Thanks. Good morning. Daniel I just want to circle back to the commentary you just had on kind of the machines and new customers versus premium per customer. I know I'm trying to simplify a very complex issue here but how does time fit into that? How would you look at those potential kind of 25 year old today that might only be looking for renters but has a lot of long-term potential to move up that kind of graduation hill and add a lot of products be that new customer growth versus somebody that might be renters today but they're also they'll add on pet today as well but maybe not go much further than that.

Answer

Yes. Hi Matt. It's great question and it gives me an opportunity to layer a little bit more of the sophistication of the system on top of my earlier comments. So before I kind of said we optimized for ROI and I left it at that dollars spent towards dollars sold but actually the machine is doing something far more sophisticated than that and it's really in line with I think the premise of your question which is not all dollars sold are born equal. Two customers can come in and both of them spend a hundred dollars and one will have a lifetime value of $50,000 because they're going to stay for a long time and increase their premiums and one can actually have a negative lifetime value because they're going to make a big claim and churn in six months and the more able, we are to predict the lifetime value the more efficiently we can deploy our cash against the appropriate or spend the CAC the customer acquisition cost in a way that optimizes the CAC LTV ratio and our data science team has been continuously improving our ability to project lifetime value of a customer based on all the parameters that make a difference.

So projecting churn, projecting up sells, projecting claims and using all of those um together. So it's not simply that we say oh renters versus homeowners we're becoming increasingly nuanced and sophisticated in the machine's ability not only to say France versus New Jersey or homeowners versus renters but to get down to a much greater level of granularity and focus as your question implies focus on lifetime value rather than on something as crude as geography or product. So all of that is happening and it's part of the systems that are learning the whole time that we're getting better and better and better at that.

6. Risks

I think it’s obvious there are some considerable risks with this investment. Lemonade are an interesting company - however we haven’t really seen anything quite like them before, making it difficult to know how this one is going to turn out.

It’s completely new.

Insurance has never worked this way before. The possibly to fall flat on their face is high.

Competitors with deep pockets will be able to adapt.

Surely the huge insurance companies will have the resources to adapt to this new method of insurance – or maybe they have too much legacy business to protect.

Business model relies on ‘graduation’ low cost renters’ into bigger ticket items. Is that a good bet?

The homeowners claims are more complicated than renters and less well suited for AI triage ($LMND ‘s only advantage).

Lemonade seem to be building a reinsurance dependence that could embed risk in its business model.

Lemonade are optimizing for growth at the moment – though in the future, they may want to be less dependant on reinsurance companies as a key part of the business model.

A similarity between Lemonade and Tesla is that shorts make up 24% and 27% of their trading volume, respectively.

The sentiment is mixed.

7. Core financials

Top line

Fourth quarter total revenue was $20.5 million, however this is somewhat misleading as the reinsurance model is shifting to ceding 75% of premiums.

In force premium grew 87% in Q4 as compared to Q4 in the prior year to $213 million. This metric captures the full scope of the top line growth before the impact of reinsurance.

Premium per customer increased 20% versus the prior year to $213. This increase was driven by a combination of increased value of policies over time as well as mix shift towards higher value homeowner and now pet policies.

Gross earned premium in Q4 increased 92% compared to the prior year of $50 million, which is in line with the increase in ‘in-force’ premium.

Gross loss ratio (kind of opposite to gross profit) was 73% for Q4, which is in line with 73% in the fourth quarter of 2019.

Profitability

Operating expenses increased just 10% in Q4 as compared to the prior year with sales and marketing expense again lower slightly due to continued improvement in our marketing efficiency.

Added new Lemonade team members in all areas of the company in support of customer and premium growth and both current and future product launches and thus saw increases in each of the other expense lines.

Global head count roughly doubled versus the prior year to 567 with a greater growth rate in customer facing departments and product development teams.

Net loss was $33.9 million in Q4 as compared to the $32.7 million reported in the fourth quarter of 2019 with a notably larger customer and in force premium base.

Adjusted EBITDA loss was $29.7 million in Q4 as compared to $31.4 million in the fourth quarter of 2019.

Balance Sheet

Cash, cash equivalence and total investments balance ended the quarter at $578 million reflecting primarily the net proceeds from the July public offering of approximately $335 million.

The company closed a successful secondary offering in January generating additional total net proceeds of approximately $640 million (this is a Q1 2021 event so not yet reflected in the financials).

Outlook

“For the first quarter we expect enforced premium at March 31 of between $241 million and $246 million. Gross earned premium between 53.5 million and 54.5 million. Revenue between $21.5 million and $22.5 million and an adjusted EBITDA loss of between $43 million and $40 million. We expect stock-based compensation expense of approximately $5 million and capital expenditures of approximately $2 million in a quarter.

And for the full year 2021, we expect in force premium at December 31 between $372 million and $378 million. Gross earned premium between $270 million and $275 million. Revenue between $114 million and $117 million and adjusted EBITDA loss between $173 million and $163 million. Stock-based compensation expense of approximately $25 million and capital expenditures of approximately $8 million in the year.”

9. Valuation

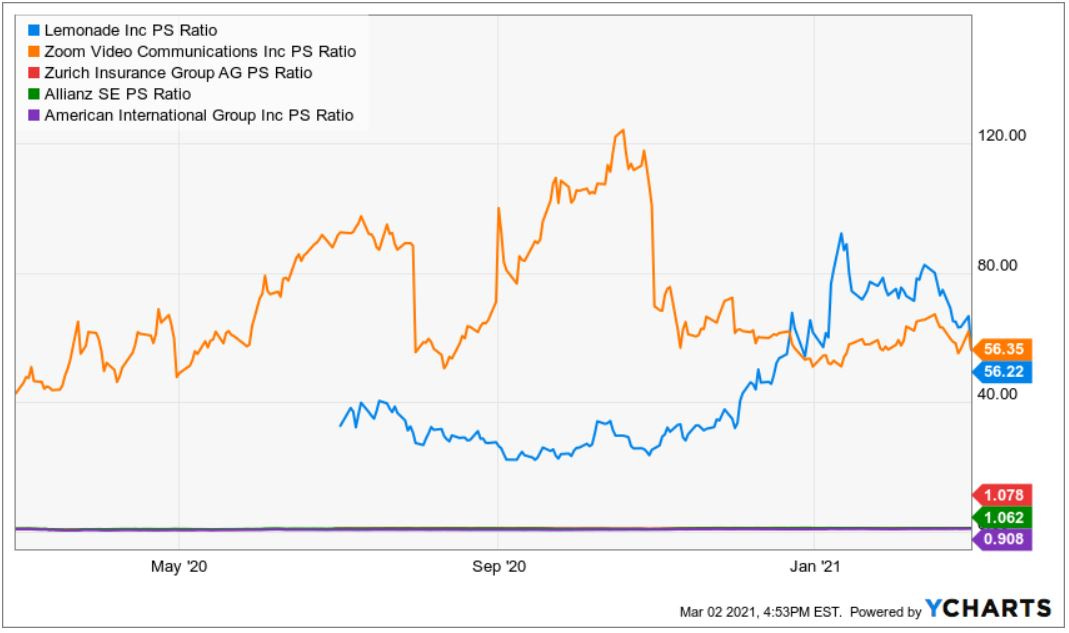

Lemonade are a strange company to value, and if I’m honest this is where most of my worries lie. They are more akin to a software company than an insurance company, which makes it hard to compare like for like. However the typical insurance company operates at a much lower multiple than lemonade’s 56X.

Is it possible that, over time, the market decides to value Lemonade more like an insurance company than it does a SaaS stock? It will be a while before we find the answer to this question. But as growth companies go, the insurance business plays out over large timescales – therefore it’s hard to say how this stock will react over the next couple of years. Will the market expect shorter-term results than Lemonade can provide?

10. Conclusion

Insurance one of the most disruptable industries in the world right now. In the past we’ve seen writing move from paper to digital, music from cassetts to CD’s to streaming, film from chemical to digital – every time an industry shifts from analogue to digital, you see customers getting an amazing experience for a fraction of the cost, you see explosive growth, and you see a changing of the guard. Insurance is going through something similar.

Lemonade hit 1,000,000 customers in only 4 years after founding. It took USAA 47 years to reach this milestone. When you see this kind of 10 x change, you can argue there is something meaningful at play.

As the flywheel spins faster and faster, and the feedback loop of more data, digital substrate and better consumer experience feed on itself – more people are going to take this opportunity seriously.

It’s still a pretty meaningful gamble to predict whether Lemonade are a game changer or just another flash-in-the-pan start-up who will fade out over time – but as soon as it becomes obvious, it will be too late.

Lemonade are about 3% of my portfolio and I’m happy with that risk/reward ratio. The industry is disruptable, but it’s still very early days for $LMND.

Cheers,

Innovestor

Great write-up!

Really bullish on this company, by the time other insurance companies will turn digital, Lemonade will have a huge head start regarding data.

Do you know perhaps, why the expected EBITDA loss for Q1 is so high? Is it because of the Texas freeze or maybe an increase in marketing?...

Can you comment a bit more on reinsurance claim process. Assume $100 earned premium and 75% loss ratio. With the current framework, how would the income statement look like? thanks